Overview- The Problem

Challenge: The bank(client) struggled with fragmented systems and labor-intensive processes for deposit client onboarding.

Goal: Implement a digital onboarding platform for quick account setup, eliminating redundant data entry, enabling eSignature for Account Agreements, and seamlessly integrating with existing legacy systems.

Strategy: The approach entailed enabling new account openings with eSignature, streamlining workflows for account agreements and data pre-filling, and directly integrating new account details into the bank's core system through web services.

This product is being developed in Temenos Journey Manager and CRM agnostic.

Process

As the project's lead designer, I collaborated closely with six developers, multiple Product Managers, and Product Owners within an Agile framework, focusing on rapid progression, frequent iterations, and product enhancement.

We operate in 2-week sprints, conducting daily UX check-ins with Product Managers and Owners to gather feedback and make immediate adjustments. Our process included regular reviews of requirements to ensure alignment with my design proposals, surpassing expectations when possible. Additionally, three-weekly meetings with the entire team facilitated smooth progress monitoring. Testing and UX refinements were ongoing and responsive to completed requirements and team insights.

For project management and documentation, we utilized Microsoft Azure DevOps, centralizing all requirements and tasks for streamlined access and updates.

Design in action

After gathering the requirements and consulting with the Product Managers and Owners, I embarked on an industry analysis, evaluating comparable products to identify appealing and unappealing features. This foundational research, combined with the specified requirements, guided my design creation process in Figma, where I developed concepts aligned with our project's vision. I expedited the preparation of these designs for prompt review and feedback sessions.

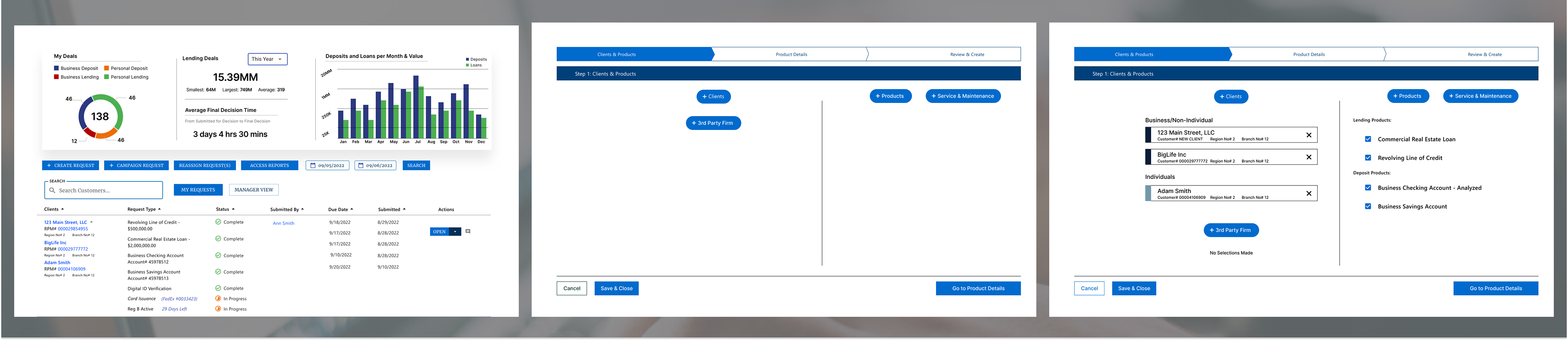

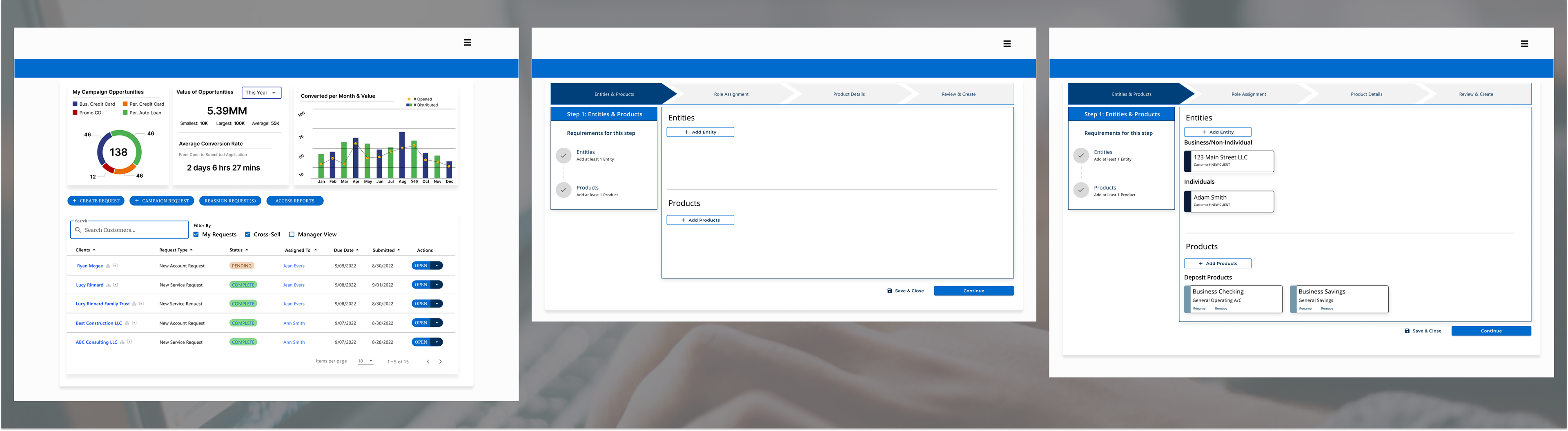

The first image showcases the Relationship Manager (RM) dashboard, a central hub for monitoring clients' account setup and opening activities. The second image depicts the product selection interface, where RMs can add clients and select products for their onboarding package, including accounts and services. The third image provides a detailed view of the chosen clients and products, illustrating the composition of the onboarding package.

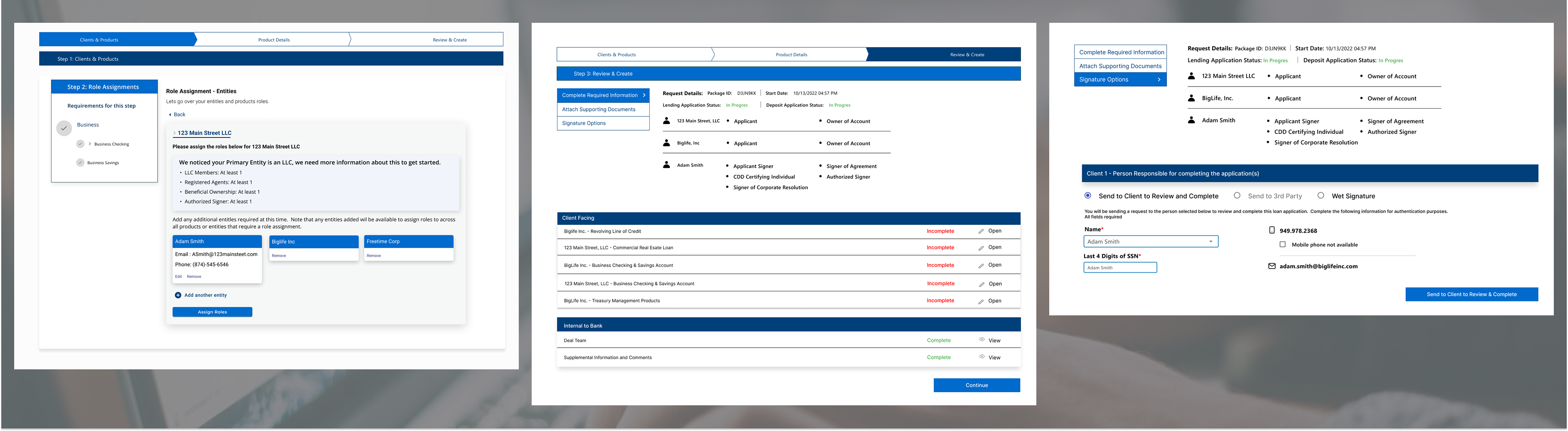

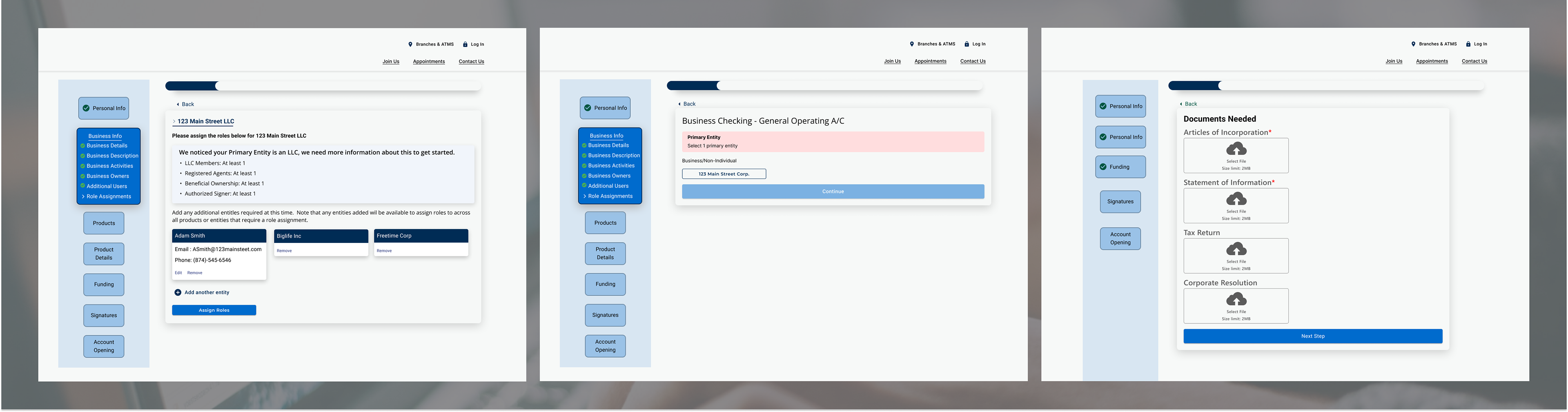

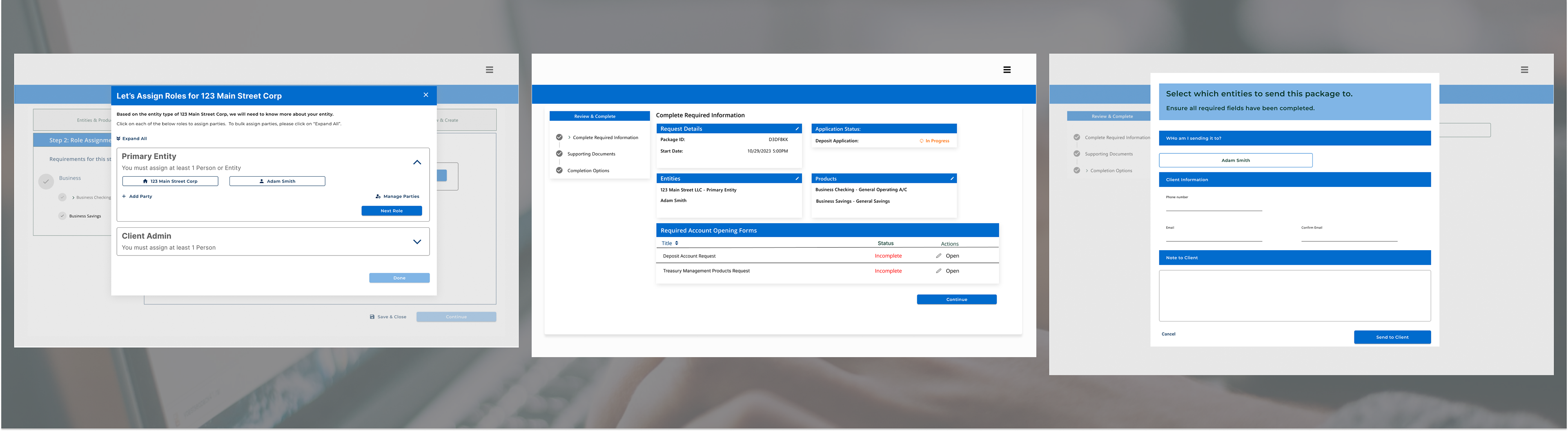

The next set of images shows how the Relationship Manager (RM) would need to assign roles to the clients added. This is the most complex piece of the process being created. It needed to be able to handle how the bank will handle companies that are owned by other companies, such as an LLC that is owned by two Corporations. How the roles of the company break down to know who would be in charge of accounts gets quite complex. The next screen was a review of what was being opened and the people or companies attached to it. Finally, how would the bank be sending the application to the client to review and sign.

Client Experience

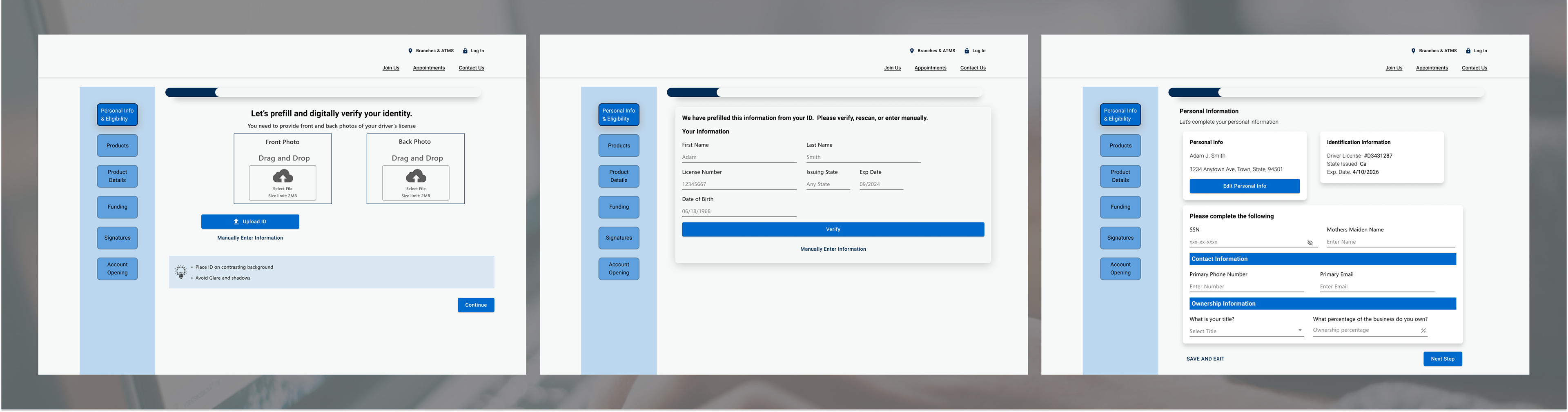

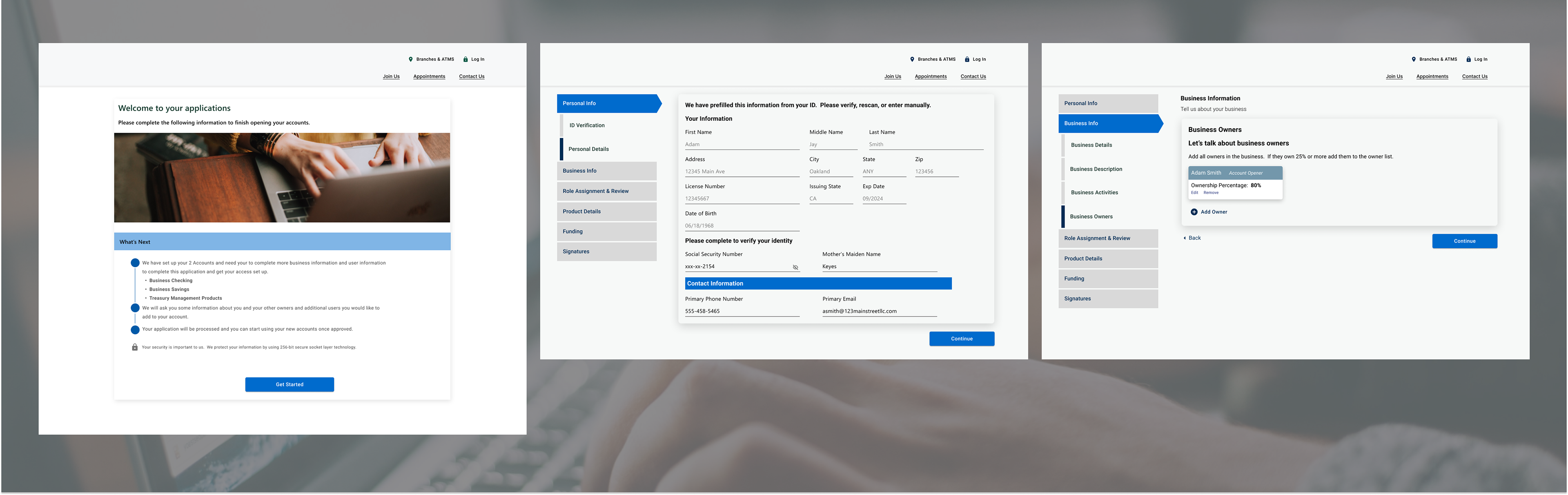

After establishing the foundational elements of the Relationship Manager (RM) interface, my focus shifted towards optimizing the client experience, particularly in completing the application process for account creation.

A pivotal aspect of this process was ID verification. In designing this step, we seized the opportunity to streamline the client's journey by pre-filling fields with previously collected data. This approach not only saved time for the client by reducing manual data entry but also leveraged the available information to minimize effort, reinforcing our commitment to efficiency and user convenience at every possible turn.

All About the Client

After the ID upload, the client is prompted to confirm the accuracy of the information. Following this verification, the process advances to the collection of business ownership details, a critical step for business checking and savings account applications. This information is essential for the bank to identify all beneficial owners of the company holding the account. The significance of this step is amplified by the potential implications of Dodd-Frank 1071 becoming law, underscoring the importance of comprehensive ownership documentation in compliance with regulatory requirements.

Role Assignments take 2

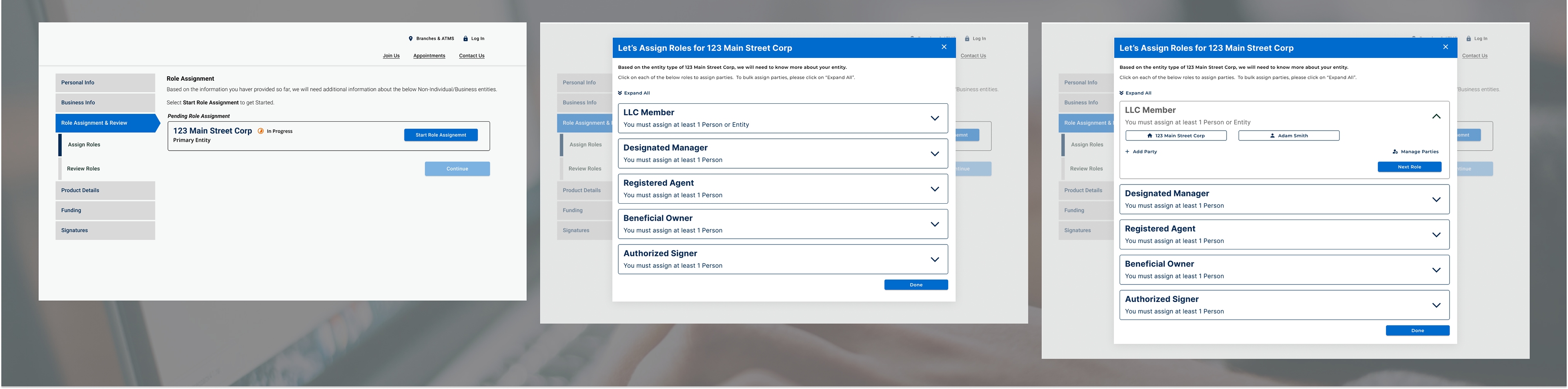

Addressing role assignments was a pivotal challenge we addressed in this project due to its inherent complexity. The bank must ascertain who is allocated to each account, along with their specific role within the account or LLC. To tackle this, we initially developed sections to exhibit the necessary roles and the methodology for their assignment.

Additionally, the upload of requisite documents forms a crucial phase of the process. The bank requires these documents not only to verify the provided information but also to fulfill legal obligations, ensuring that all necessary compliance and regulatory standards are met.

Its all about Iterations

In the dynamic environment of Agile project management, where designs and requirements frequently evolve, our priority was to ensure maximum flexibility in our designs. I aimed to create components that were highly reusable, enabling developers to efficiently incorporate them into a component library and adapt content as necessary. This was achieved through extensive feedback sessions with Product Owners and by involving developers in these discussions, ensuring they were always informed and could seamlessly integrate design changes.

Roll the Updates

Throughout the project, updates encompassed everything from layout adjustments to navigation modifications, yet the core process stayed intact. These UI changes were the result of numerous sprints and extensive discussions among team members. This collaborative effort ensured that all requirements were fulfilled and that the flow was optimized for every use case and objective.

A note on mobile

It's crucial to recognize that the banking interface(banker facing) is designed exclusively for desktop use, with the layouts and functionalities tailored to this environment. On the other hand, the client interface, although primarily expected to be accessed via desktop, has been crafted with responsive design principles to ensure a seamless experience on mobile devices as well. This dual approach ensures that both bankers and clients can interact with the system effectively, regardless of the device used.